Just a week ago, China was facing a banking system crisis that necessitated an injection of 375 billion yuan ($53 billion) into the money market, and that was after the prior week’s injection of 250 billion yuan ($36 billion). But now, after Christmas has passed, the crisis seems to be abating. That is good news for bond prices worldwide, including in the U.S.

And the resolution was foretold by copper prices, which is the really cool part of this.

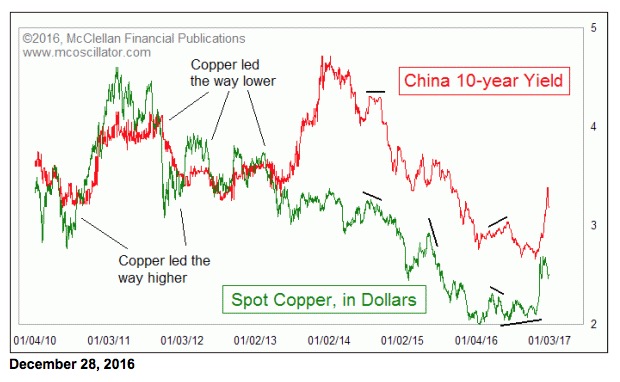

This week’s chart compares spot copper prices to the yield on the Chinese 10-year government bond. There is an obvious correlation, which is nice to know, but that is not what is interesting. Finding two data series which behave exactly like each other is terribly boring. There is no insight there. The fun comes when there are two data series that are almost the same, but one is slightly different, and that one gives insights about the other.

Such is the case with copper versus Chinese bond yields. It is also the case with gold prices measured in euros versus dollars, for example. When the two series disagree, one is the expert about where both are headed. Such is the case with copper prices foretelling moves in Chinese bond yields.

Most of the time, the two move together. But occasionally they disagree, as is the case just recently with copper prices refusing to confirm the higher Chinese bond yields. That was a tell that the Chinese bond rate blowoff was nearing an end.

If China’s yield melt-up is really all done, as copper suggests, then so should be the same melt-up in U.S. 10-year yields.

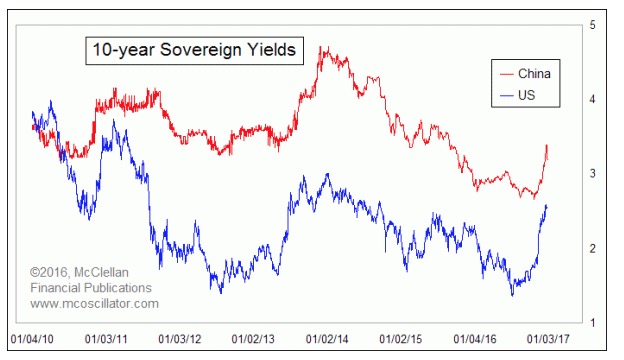

The two countries’ bond yields tend to dance the same dance steps, more or less. The U.S. 10-year yield has danced a little bit farther on this recent up move than China’s did. Accordingly, it has farther to fall back again on the reversal.

Tom McClellan

The McClellan Market Report

www.mcoscillator.com